Insurance innovation is not failing - Core systems are holding it back

Share this Article on

TL;DR

Insurance innovation often shows promise in pilots, whether in claims automation, underwriting intelligence, or digital customer experiences, yet many initiatives struggle to scale across lines of business, products, and regulatory environments. This article explores why pilot success breaks down in insurance organizations and what it takes to transform legacy-driven operations into enterprise-wide sustainable modern operations.

Across the insurance industry, innovation activity has been high since Covid-19. Pilot projects are launched around automation, advanced analytics, AI-assisted decision making, and digital customer journeys. While many demonstrate early promise, few translate into sustained, enterprise-wide impact.

This pattern is not coincidental. It reflects a structural disconnect between how project-level pilots are initiated and how large insurance organizations are designed to operate. The failure point is not experimentation itself, but the absence of an operating model that allows innovation to coexist with core insurance complexity.

The structural limitation of pilot-led innovation

Pilots are, by definition, optimized for speed and containment. They operate within narrow functional boundaries, limited data sets, and controlled risk exposure. This makes them effective for validation, but poor predictors of scalability.

What pilots typically do not account for is the full operational reality of an insurer: tightly coupled legacy systems, jurisdiction-specific regulatory logic, product configuration dependencies, rating logic, bordereaux flows, broker and agent workflows, delegated authority models, and exception-driven processes.

For example, a pilot in claims automation may demonstrate faster processing within a single line of business. Scaling that capability requires alignment with:

- Claims workflows across multiple products (P&C, specialty lines, etc.)

- Regulatory reporting requirements in different jurisdictions

- Downstream impacts on reserving and actuarial calculations

When a pilot is expanded beyond its initial scope, these constraints surface quickly, often eroding the very benefits that justified the initiative.

As a result, innovation stalls not because it lacks value, but because it lacks an execution model designed for scale.

Legacy systems define the scaling constraint

For most insurers, legacy platforms remain central to core operations. Policy administration, billing, claims, underwriting, and reporting systems have evolved over decades, embedding business logic, regulatory rules, and operational workflows deep into the technology stack.

Innovation efforts frequently underestimate this reality. New capabilities are layered on top of existing systems without sufficient architectural alignment, creating fragile integrations, and increasing operational risk. While this approach may be sufficient for pilots, it rarely supports enterprise-wide deployment.

In many carriers, these systems sit within established ecosystems such as Guidewire or Duck Creek, where:

- Product definitions are tightly coupled with system workflows

- Regulatory requirements, rating rules, and product configuration logic are embedded at the system level

- Changes require coordinated releases across multiple functions

In this environment, even a focused change can have a wider operational footprint. A new digital capability may need to work across FNOL, policy servicing, billing, claims reserves, regulatory filings, and reporting controls before it can be considered scalable.

Scaling transformation requires working with legacy systems deliberately, not bypassing them, and not attempting wholesale replacement, but modernizing how they interact with new capabilities.

As transformation efforts push into core legacy systems, scaling introduces organizational consequences that technology teams alone cannot absorb. Decisions around risk, compliance, and operating impact become intertwined with architectural choices. This is where scaling begins to demand enterprise-level ownership.

Why scaling is an executive problem, not a technology one

The transition from pilot to scale is not primarily a technical hurdle. It is a leadership and governance challenge. At scale, innovation impacts core insurance outcomes:

- Underwriting performance and loss ratios

- Claims leakage and operational costs

- Regulatory compliance and reporting exposure

These impacts bring multiple leadership roles into the equation — underwriting, claims, actuarial, risk, compliance, operations, and distribution — making alignment essential.

In markets like the US, changes may need to align with state-level regulatory expectations. In Europe, scaling across countries introduces additional coordination complexity. What begins as a localized innovation quickly becomes an enterprise accountability issue.

Without this alignment, pilots remain in disconnected initiatives zone rather than building blocks of transformation.

Business process readiness: the silent determinant of transformation success

System modernization inevitably reshapes how business decisions are executed, not just how transactions are processed. Even when the technology uplift is sound, misalignment at the process level can dilute outcomes.

A critical enabler is early clarity on process impact mapping current (As-Is) workflows against the future-state (To-Be) operating model the new system introduces. This allows organizations to assess where decision authority shifts, controls are redefined, or operational handoffs change, and to secure business sign-off before these changes are embedded into the platform.

Treating process alignment as a governance activity, not a change-management afterthought accelerates adoption, reduces friction at go-live, and ensures the technology investment translates into sustained operational value. In insurance, this is particularly critical where process changes affect:

- Underwriting authority and exception handling

- Claims adjudication and escalation pathways

- Interactions with broker and agent workflows

What enables scaling transformation

Insurers that successfully scale innovation adopt a fundamentally different approach.

They anchor innovation initiatives to an enterprise transformation blueprint, ensuring that pilots align with long-term architectural and operational objectives. They focus on decoupling business logic, enabling API-driven integration, and establishing consistent data flows across policy, claims, underwriting, billing, and reporting so new capabilities can scale without destabilizing core systems.

Compliance, auditability, and control are embedded into solution design from the outset, reducing friction as initiatives expand across products and geographies. Value realization is tracked continuously, with clear metrics tied to operational efficiency, risk management, and business agility.

Most importantly, innovation is treated as a capability to be institutionalized, not a series of experiments to be evaluated in isolation.

Moving from pilots to sustainable advantage

When transformation is approached this way, innovation stops stalling. Capabilities scale predictably. Change becomes less disruptive. The organization gains the ability to evolve continuously rather than episodically.

This is where insurance modernization delivers its intended outcome: not isolated success stories, but a durable competitive advantage.

Enabling scalable insurance digital transformation

Insurers that succeed in moving beyond pilot-driven innovation align strategy, architecture, and execution to scale transformation across both legacy and modern environments delivering measurable business outcomes. At Aspire Systems, we partner with insurers to help them build insurance innovation strategy with confidence and succeed in enterprise-scale digital transformation.

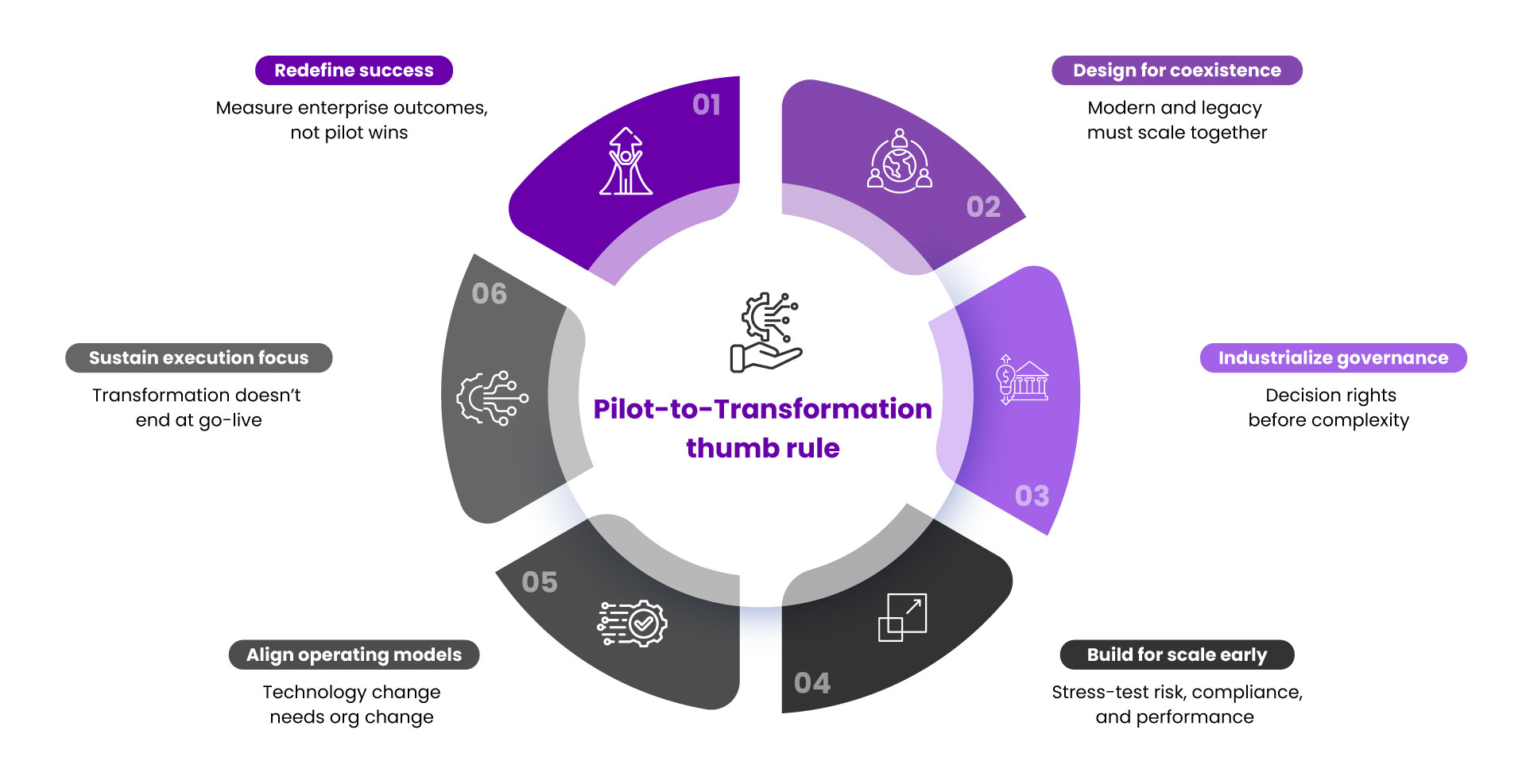

For insurers evaluating whether an innovation initiative is ready to move beyond pilot mode, the following thumb rule can serve as a practical checkpoint before enterprise rollout.

Explore how Aspire Systems helps insurers modernize core systems and scale digital transformation with confidence.

Customer story: Aspire Systems helped a global risk management products and services provider to modernize its digital ecosystem through end-to-end digital engineering services, enhancing customer experiences, optimizing claims operations, and strengthening fraud prevention. Read case study

References

1. McKinsey report: Losing from day one: Why even successful transformations fall short

In This Article

- The structural limitation of pilot-led innovation

- Legacy systems define the scaling constraint

- Why scaling is an executive problem, not a technology one

- What enables scaling transformation

- Moving from pilots to sustainable advantage

- Enabling scalable insurance digital transformation